Research

Working Papers

Local Projections vs. VARs for structural parameter estimation

Abstract

This paper conducts a Monte Carlo study to examine the small sample performance of IRF matching and Indirect Inference estimators that target impulse responses (IRFs) that have been estimated with Local Projections (LP) or Vector Autoregressions (VAR). The analysis considers various identification schemes for the shocks and several variants of LP and VAR estimators. Results show that the lower bias from LP responses is a big advantage when it comes to IRF matching, while the lower variance from VAR is desirable for Indirect Inference applications as it is robust to the higher bias of VAR-IRFs. Overall, I argue that Indirect Inference outperforms IRF matching when estimating Dynamic Stochastic General Equilibrium (DSGE) models as the former is robust to potential misspecification coming from invalid identification assumptions, small sample issues or incorrect lag selection.

Presented @ Bank of Canada (20th Dynare Annual Conference), European University Institute (5th EUI Alumni Conference in Economics, Macro WG & Cooper WG), Bank of England (Macro Brownbag Seminar), Barcelona School of Economics (BSE Summer Forum 2023), ESCP Business School (T2M 2023), ADEIT University of Valencia (SAEe 2022), European Central Bank (RCC5 Brownbag Seminar)

A previous version of this paper was circulated under the title “Indirect Inference: A Local Projection Approach" and co-authored with Russell W. Cooper

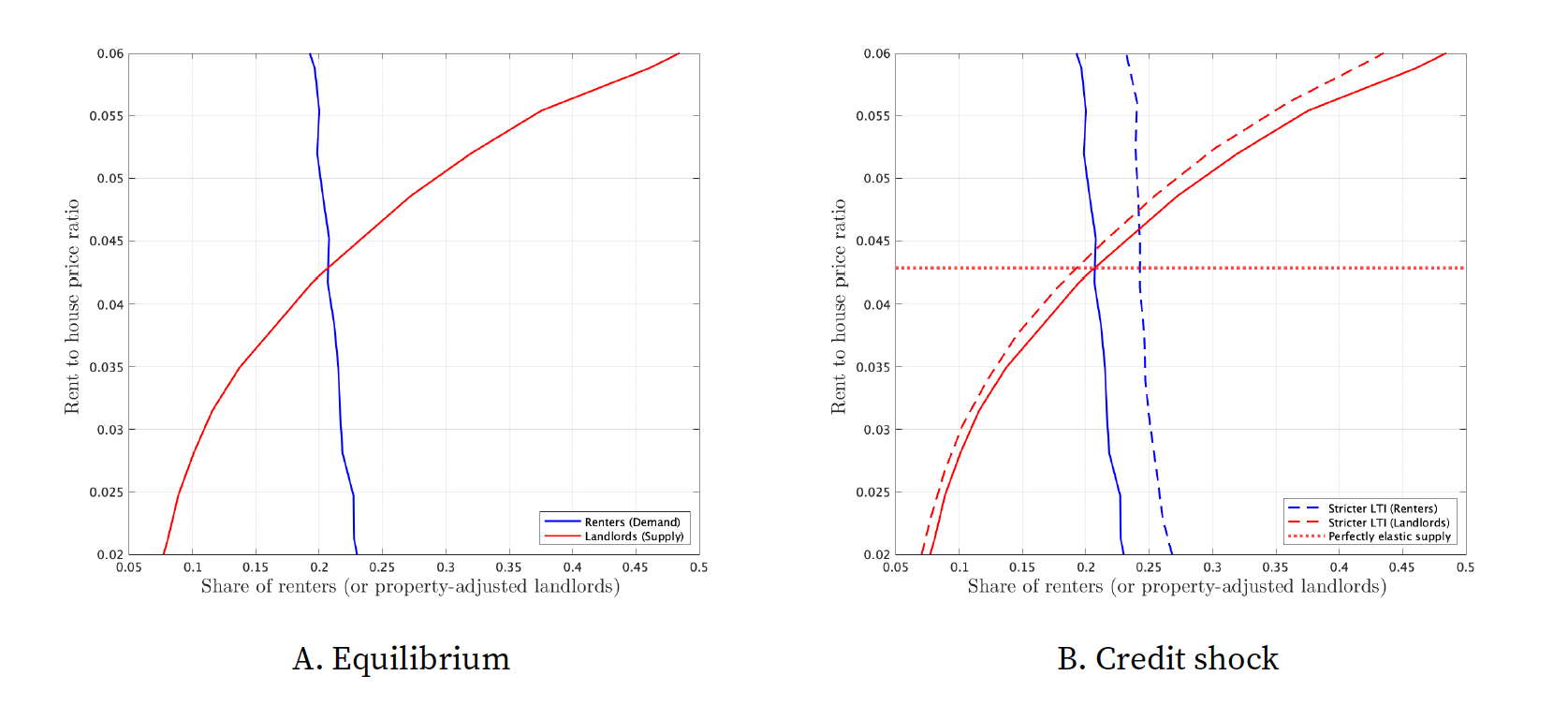

The aggregate and distributional implications of credit shocks on housing and rental markets (with Andrew Hannon & Gonzalo Paz-Pardo)

Abstract

We build a model of the aggregate housing and rental markets in which house prices and rents are determined endogenously. Households can choose their housing tenure status (renters, homeowners, or landlords) and the size of their homes depending on their age, income and wealth. We use our model to study the impact of changes in credit conditions on house prices, rents and household welfare. We analyse the introduction in Ireland in 2015 of policies that limited loan-to-value (LTV) and loan-to-income (LTI) ratios of newly originated mortgages and find that, consistently with empirical evidence, they mitigate house price growth but increase rents. Homeownership rates drop, and young and middle-income households are negatively affected by the reform. An unexpected permanent rise in real interest rates has similar effects – by making mortgages more expensive and alternative investments more attractive for landlords, it increases rents relative to house prices.

Presented @ U of Reading (2025 MMF), King's College London (2025 EAYE), Universidad Torcuato Di Tella (2024 SED Winter Meeting), XXVII Workshop on Dynamic Macroeconomics (Vigo), Queen Mary University of London (6th Economics & Finance Workshop), Bank of Spain, University of Amsterdam (T2M 2024), University of Salamanca (SAEe 2023), Bank of England (FSSR Brownbag Seminar), London Business School (TADC Economics 2023), European University Institute (Macro WG, 4th Year Forum & Cooper WG), 2025 SAET$^{\star}$, 2025 Columbia-NYU-Yale Housing Day$^{\star}$, 2024 Lisbon Housing, Monetary Policy and Inequality Workshop$^{\star}$, University of Mannheim$^{\star}$, University of Vienna$^{\star}$, Sveriges Riksbank$^{\star}$, Catolica Lisbon SBE (Lisbon Macro Workshop 2023)$^{\star}$, Bank of Ireland$^{\star}$, European Central Bank (DG Monetary Policy, DG Research & RTF on Heterogeneity)$^{\star}$, Toulouse School of Economics (ECHOPPE 2023)$^{\star}$, Paris School of Economics$^{\star}$, Norges Bank$^{\star}$, BI Norwegian Business School$^{\star}$, St. Gallen$^{\star}$

Media Coverage: The Economist || Irish Independent || Irish Examiner

Work in Progress

The role of interest fixation periods for macro-prudential & monetary policies (with Stephen Millard & Alexandra Varadi)

Abstract

In many countries the most common mortgage contract neither has a fixed nor a fully adjustable rate. The typical interest fixation period varies between two to ten years. This paper offers a structural analysis of how the interest rate fixation period affects the transmission of monetary policy and how it interacts with borrower-based macro-prudential limits. Using a general equilibrium model with long-term debt and calibrated to the United Kingdom, we find that: (i) the interest fixation period and the tightness of credit conditions do not matter if monetary policy shocks are transitory, (ii) looser credit limits and shorter fixation periods amplify the redistributive effects of inflation target shocks that increase nominal rates persistently, and (iii) LTV limits act as a backstop to the high sensitivity of PTI limits to monetary policy, specially when the interest fixation period is short.

Presented @ Czech National Bank (Second Annual Conference), Bordeaux School of Economics (2025 EEA Congress), Bank of England (FSSR Brownbag Seminar), U of Reading (2025 MMF)$^{\star}$, NIESR$^{\star}$

Lumpy Durable Goods, Intertemporal MPX, and Policy Transmission (with David McCarthy)

Dormant Projects

Average Inflation Forecast Targeting (with Sebastian Schmidt)

Durables and Portfolio Choice: Response to Aggregate Shocks (with Russell W. Cooper & Sebastian Rast)

$^\star$ Presentation given by a co-author.